Monetary policy always had an air of the mystical. The past is filled with fallen sages like Alan Greenspan, inflation-warriors like Paul Volcker and gurus like Milton Friedman.

Yet, no central bank has ever elevated mythology quite like the Reserve Bank of New Zealand.

Whether the Kiwi central bank’s spiritualism will help it fight the stagflation monster is a different question.

International analysts might be confused by the publications coming out of the RBNZ. Where other central banks produce sober-looking documents, the RBNZ’s latest annual report could almost pass for a tourism promotion brochure. Beautiful pictures of nature, colourful illustrations, smiling children, kayakers and office workers grace the pages.

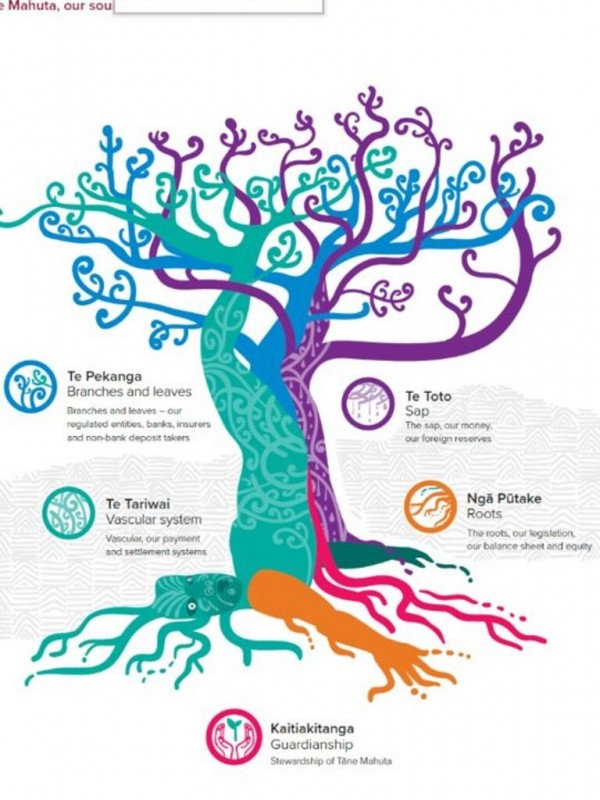

The centrepiece in this collage is Tāne Mahuta, the fabled tree god of Māori mythology. The RBNZ has chosen him to represent its chosen purpose: “For many decades Te Pūtea Matua, the Reserve Bank of New Zealand, has stood as kaitiaki (guardian) to Tāne Mahuta, the financial ecosystem of Aotearoa”, the Bank tells us.

And so, the RBNZ explains its role with terms like ‘Te Toto – Sap’ when they refer to “our money, our foreign reserves”. Or ‘Te Tariwai’, meaning the vascular system, where other central banks would talk about payment and settlement systems.

This would all be quirky but harmless if it was just some marketing gloss applied to a conventional central bank.

Unfortunately, there is nothing conventional about the RBNZ anymore. And that is biting the bank now that it has to defend faith in the Kiwi dollar.

Until a few years ago, the RBNZ was a central bank like many others: led by bureaucrats, speaking the language of finance, and almost as intent on being boring as on pursuing its single objective: price stability.

All that changed when New Zealand elected a new government in 2017. First, the Labour-led coalition appointed a flamboyant new governor, Adrian Orr. Then it tasked the RBNZ with also keeping an eye on house prices. And finally, it widened its formal mandate to include “maximum sustainable employment”.

The combination of the three has revolutionised New Zealand central banking.

Since his appointment in early 2018, Governor Orr has made his mark on every aspect of the RBNZ. A new Tāne Mahuta inspired logo replaced the RBNZ’s old coat of arms. The Bank created an international Network for Indigenous Inclusion. It published its own climate change strategy. It told the government about its expectations for infrastructure investment. All worthwhile objectives, of course, just not what a conventional central bank would do.

RBNZ’s expanding portfolio of activities led to an explosion in staff. The RBNZ’s personnel numbers have climbed from 255 full-time equivalents in 2018 to 411 in 2021 – or from $32 million to $54.3 million in salaries.

The problem with the RBNZ’s growth is not just that it has turned its attention to political issues for which it has no primary responsibility. At the same time, it has neglected its core mandate. As an example, in its last Annual Report, published in October 2021, it used the word ‘climate’ 45 times and ‘carbon’ 23 times. On the other hand, ‘inflation’ got only 14 mentions and ‘price stability’ a mere four.

Not all the RBNZ’s confusion is the Bank’s fault, though. Minister of Finance Grant Robertson has to take some responsibility, too. For it was Robertson who gave the RBNZ the so-called dual mandate of price stability and full employment.

Economists have known since the 1970s that central banks cannot choose between inflation and unemployment (at least not in the long run). The wide consensus of the profession is that central banks should target inflation – and only inflation. Nevertheless, the New Zealand Government imposed an employment target on the RBNZ.

This has made the RBNZ err on the side of stimulus. Especially during the Covid crisis, the RBNZ embarked on one of the most aggressive programs of quantitative easing (vulgo: money printing) anywhere in the world.

The result of all these distractions is a New Zealand inflation rate that has now shot up to 6.9 per cent. It would have been even higher had the Government not artificially lowered fuel prices through a temporary fuel duty cut.

As the RBNZ now frantically lifts its cash rate to quell the inflation storm, it realises substantial losses on the assets it purchased with its earlier quantitative easing program.

Fortunately for the RBNZ, the Government has indemnified it against all such losses (currently more than NZ$8.3 billion). Without it, the Bank would now be in negative equity to the tune of 6 per cent of its balance sheet. Unfortunately, the RBNZ’s indemnity means that means taxpayers must now pay for these losses.

New Zealand faces a significant monetary challenge. Inflationary pressures are being exacerbated by the government’s continued increase in expenditures, as shown in last week’s Budget.

Meanwhile, thanks to all of its political activism, the RBNZ has lost its street cred for maintaining price stability. That means the RBNZ has to work doubly hard to rein in inflation. It needs to overcome its self-inflicted reputational issues while also counteracting the government’s fiscal stimulus.

In Māori mythology, the hero Māui once used a magic jawbone to slow the sun. If New Zealand is to avoid galloping inflation, the RBNZ governor will need to devise some similar trickery soon.

And if he cannot do that, conventional economics might help.